ERP vs. Standalone Property Management Software: A Comparison

Key Takeaways

- Property management software works well for smaller portfolios where rent collection, maintenance, and basic lease tracking are all that is needed.

- ERP adds the financial layer that PM software does not include, such as a general ledger, multi-entity accounting, and audit-ready reporting.

- Most teams notice the gap during month-end close when two systems show different numbers for the same period.

- PM software and ERP can run together as long as they share a live connection rather than a manual data transfer.

- The right choice depends on the size and structure of the portfolio, not on which software has the longer feature list.

In the age of sail, ships carried two navigators who calculated position independently. The thinking was simple: if both charts agreed, the ship was on course. If they disagreed, the captain had a serious problem on his hands.

Most real estate finance teams are still running this system today.

One number comes from the property management platform. A different number comes from the accounting system. Someone senior looks at both and decides which one to trust before the board meeting. Sometimes they match. When they do not, the next few hours disappear into finding out why.

This is the moment that brings most growing real estate businesses to the property management software vs ERP software comparison. Not a planned technology review. Not a budget cycle. A specific breakdown in how data moves between systems, and the realization that the team has been reconciling two sources of truth every single month without anyone deciding that was acceptable.

Both types of software do useful work. Understanding the difference between ERP and property management software comes down to what each one stops doing, and whether the portfolio needs the part the other one covers.

Deloitte’s 2026 commercial real estate outlook found that most global real estate leaders expect stronger revenue through 2026, but also pointed out that results depend heavily on data quality and how well operations are managed (source). The gap between PM software and ERP is a gap in exactly those two areas.

Why Do Real Estate Teams Start Comparing These Two?

Teams rarely go looking for this comparison on their own. Something in the current setup stops working, and the search begins.

Here are the most common triggers:

- Pulling reports for an investor who wants financials split by property, entity, and fund, and realizing the current system cannot produce that without exporting to a spreadsheet first.

- A lease change that saved correctly in the PM platform but never reached the accounting system, because the two tools sync once a night and not in real time.

- A month-end close that keeps running longer than it should because someone has to manually reconcile data from two separate systems.

These are not signs that the property management software is broken. They are signs that the portfolio has grown past what the PM tool was originally set up to handle.

What Does Property Management Software Do Well?

Property management software is good at what it was designed for. Before these tools existed, managing a rental portfolio meant paper rent checks, phone calls for maintenance, and letters in the post for tenant communication.

Today, a well-configured PM tool handles all of this automatically:

- Rent collection: online payment portals, automated reminders, and payment tracking at the tenant level

- Maintenance requests: logged, assigned to the right person, tracked to completion, with a full history on record

- Tenant communication: a portal where residents can pay, submit requests, and check their lease details without calling the office

- Lease tracking: renewal dates surfaced before they pass, basic lease terms stored and accessible

For a portfolio with one legal entity, one set of books, and no outside investors expecting regular reports, a solid PM tool paired with something like QuickBooks handles the job well. If you are evaluating PM platforms specifically, the full comparison of property management CRM options covers how they differ on these core functions. Not every portfolio needs to go further than this.

Where Does Property Management Software Fall Short?

The limits tend to appear in three specific areas. Which one shows up first depends on how the portfolio is structured.

Financial Reporting Gets Harder as the Portfolio Grows

PM software reports are designed around individual properties. Occupancy rates, rent rolls, basic income and expenses per building. For day-to-day management, that is usually enough.

The problem starts when the portfolio needs reports that cross entities:

- A consolidated income statement across multiple legal entities

- Financials that separate results by fund, property, and ownership structure at the same time

- Lease accounting reports that comply with ASC 842 or IFRS 16

At that point, the PM tool runs out of road. The only option is to export the data and build the report manually in a spreadsheet, which takes time and creates room for errors.

Managing Multiple Entities Becomes a Manual Job

As a real estate business grows, it almost always ends up with more than one legal entity. Different properties fall under different ownership structures. Fund vehicles get added. Some holdings are in different regions with different requirements.

Most PM software sees the whole portfolio as one thing. It does not split records cleanly by entity or produce separate books for each one while still showing a combined view at the top. That kind of structure is what ERP is built for, and PM software was not.

The Audit Trail Is Too Basic

A basic PM tool records who logged in and when. That is not enough for an audit.

A proper audit trail tracks every financial entry from start to finish. It shows who created it, who approved it, what changed, and when each step happened. Affordable housing operators, community associations, and portfolios that face regular external reviews find this gap first, usually when an auditor asks a question that the system cannot answer.

What Does ERP Add That Property Management Software Does Not?

ERP does not replace property management software. It adds the financial layer that runs underneath it.

That layer includes:

- A general ledger that handles real estate-specific transactions natively

- Separate books for each legal entity, with a consolidated view across all of them

- An audit trail that traces every financial entry back to its source

- Reports that pull live data and segment by property, entity, fund, and currency

When a portfolio uses the Propertese NetSuite integration, all of this runs on enterprise-grade accounting infrastructure. A lease change posts to the right entity’s books automatically. No one has to enter the same information twice into two different systems.

This also improves the quality of financial data for more complex decisions. Good financial analysis, such as building a DCF model with the right discount rate for real estate investments, only works when the underlying numbers are clean and traceable. That level of data quality comes from having every transaction in one system, not spread across several.

The reporting that comes with an ERP-connected platform is also a different product from what PM software offers. Instead of property snapshots, it produces income statements, balance sheets, and cash flow summaries broken down by subsidiary, property, and unit, pulling from data that updates in real time.

ERP vs Property Management System: Side by Side

| Capability | Standalone PM Software | ERP-Connected Platform |

| Rent collection | Strong, with online portals | Included, entries post to the ledger automatically |

| Maintenance and work orders | Strong, with tenant-facing portals | Included, costs flow to the correct entity and property |

| Lease tracking and renewals | Standard feature | Included, with ASC 842 and IFRS 16 entries posting automatically |

| General ledger | Requires a separate accounting tool | Built-in, updates in real time |

| Multi-entity accounting | Rare or manual | Core feature, managed from one login |

| Investor and owner reporting | Basic, often requires manual assembly | Built into the reporting layer, segmented by entity and fund |

| Audit trail | Basic login and activity logs | Full entry-level trace, every change recorded |

| Multi-currency | Rare | Transaction-level conversion |

PM software covers the top three rows well. ERP covers all eight. The question is which rows the portfolio actually needs.

When Should a Portfolio Stick With Property Management Software?

For a lot of real estate businesses, property management software is not a temporary solution. It is the right long-term fit.

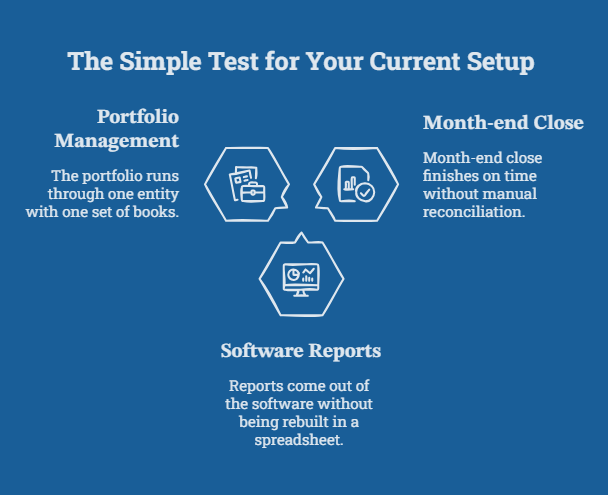

A portfolio with one legal entity, fewer than a hundred units, and a finance team that closes the books in QuickBooks or Xero without any trouble does not need ERP. The added complexity would not pay off at that scale.

The same is true for property managers who look after a small number of buildings for one owner and have no investor reporting requirements. A PM tool with a good export function handles what they need.

A simple way to check if the current setup is still the right fit:

If all three of those are true, the current setup is working.

When Does ERP Become the Better Choice?

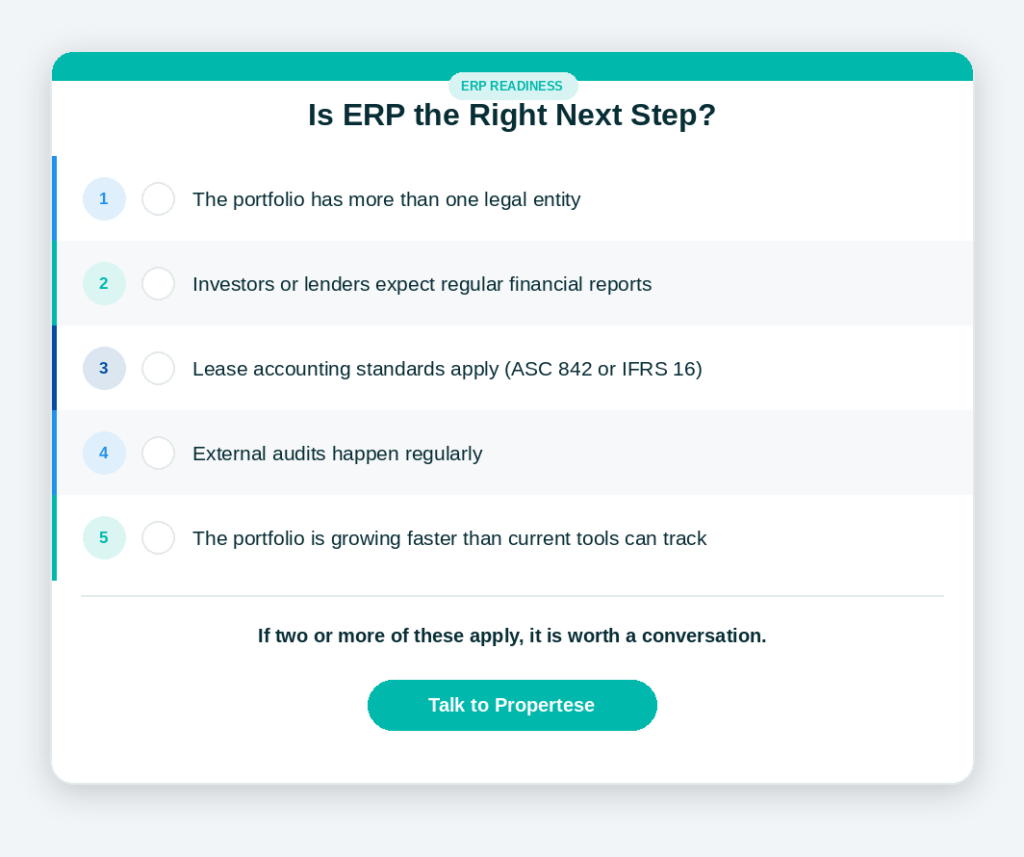

The shift from property management vs ERP software usually happens when a few of these conditions appear together rather than just one at a time.

- The portfolio has more than one legal entity. When properties are held under different entities, each one needs its own set of books. ERP handles this from a single login through subsidiary management, keeping each entity’s records separate while showing a combined view across all of them. Most PM tools cannot do this without workarounds.

2. Investors or lenders expect regular financial reports. When outside parties need financial statements on a fixed schedule, there is no time for manual report-building. An ERP platform produces those reports directly, without an export step.

3. Lease accounting standards apply. ASC 842 and IFRS 16 require specific entries every time a lease is modified, renewed, or ended early. Tracking these manually in a spreadsheet alongside a PM tool works until it doesn’t. An ERP-connected platform handles those entries as part of the lease event.

4. External audits happen regularly. For portfolios that face annual or more frequent audits, every financial entry needs to be traceable to its source. A PM tool activity log does not meet that standard.

5. The portfolio is growing quickly. When more entities, properties, and reporting requirements are being added each year, waiting to switch gets more expensive over time. The longer the team relies on workarounds, the harder the migration becomes.

Frequently Asked Questions

Can PM software and ERP work together?

Yes. Some portfolios use PM software for daily operations and connect it to ERP for the financial layer. The connection needs to be a live integration, not a nightly data file. A CSV export that runs once a day is not the same as a real-time sync.

What is the difference between ERP and real estate management software?

ERP is the broader category. It includes the general ledger, multi-entity accounting, compliance, and reporting infrastructure. The ERP vs real estate management software distinction usually comes down to one question: is the general ledger built into the platform or does it require a separate tool?

Is ERP too much for a small portfolio?

For many small portfolios, yes. A single-entity portfolio with simple accounting needs works well with PM software plus QuickBooks or Xero. ERP makes more sense once multiple entities, investor reporting, or lease accounting compliance come into the picture.

What does migrating from PM software to ERP actually involve?

The biggest delays come from messy data. Duplicate records, inconsistent naming, and lease history that only exists in spreadsheets all slow things down. Cleaning the data before the migration starts consistently saves more time than it costs.

Do all ERP systems work for real estate?

No. General-purpose ERP systems cover accounting infrastructure but leave out real estate-specific functions like rent roll management, lease tracking, and maintenance workflows. A real estate ERP, or a PM platform connected to an ERP like Propertese, covers both layers.

Conclusion

The property management software vs ERP software decision does not have a single right answer. It depends on how the portfolio is structured, what the reporting requirements are, and whether the current setup is creating problems that keep getting bigger.

If month-end close runs well and reports come out of the system without extra work, the current setup is doing its job. If those things are starting to slip, that is worth a direct conversation rather than another workaround.

Talk to Propertese about where the portfolio stands and whether a different setup would actually change things.