Rent Roll Management Best Practices in Real Estate

Key Takeaways

- A rent roll that has not been updated since the last lease amendment is a liability, not an asset.

- Missed escalations and incorrect CAM allocations compound quietly for months before showing up in a reconciliation, making them the most expensive rent roll errors to fix.

- Manual rent roll management typically works until around five to ten properties or the first investor reporting obligation, whichever comes first.

- Commercial rent roll best practices require NNN lease structures, percentage rent clauses, and CAM recovery pools to all be tracked in the rent roll itself, not in separate spreadsheets.

- Rent roll software connected to the general ledger eliminates the gap between what the lease says and what the books record.

In commercial real estate, a six-month-old rent roll amendment can cost more than the legal fees to create it. A tenant signs a lease amendment in March changing their escalation schedule. The amendment gets filed. The rent roll does not get updated. By September, the tenant has been paying below their contracted rate for six months, the discrepancy is buried in three months of bank statements, and untangling it takes days.

Rent roll errors do not announce themselves. They build quietly in the gap between what the lease document says and what the tracking system shows. The longer that gap stays open, the more expensive it becomes to close.

Rent roll management best practices in real estate come down to one goal: keeping that gap at zero. This post covers what a rent roll should contain, how to keep it accurate, how to analyze it, and when spreadsheets stop being the right tool.

What Is a Rent Roll in Real Estate?

A rent roll lists every tenancy in a property or portfolio. It shows the current rent each tenant pays, the lease term, and the key financial terms of each lease. It is the primary financial summary of a portfolio’s income-generating capacity.

Investors use it to assess portfolio value, and lenders use it for underwriting. Property managers use it to track rent collection and lease events. For any of these uses to be reliable, the rent roll must reflect the current state of every lease. That includes all amendments, renewals, and modifications since the original document was signed.

A rent roll is different from a lease abstract. A lease abstract extracts all the key terms from a single lease. A rent roll aggregates a summary of those terms across every tenancy in the portfolio. Both need to be current. But the rent roll is the live financial view.

What Should a Real Estate Rent Roll Include?

A complete real estate rent roll contains more than just the current rent amount. For each tenancy, it should capture:

Core lease terms:

- Tenant name and unit or suite number

- Lease start and end date

- Monthly or annual base rent

- Rent escalation schedule and next escalation date

- Renewal options and notice deadlines

Financial terms:

- Security deposit amount and conditions

- Tenant improvement allowance and amortization schedule

- Free-rent period dates

- Current rent versus market rent comparison

For commercial leases, additionally:

- Lease type (gross, modified gross, NNN, or percentage rent)

- CAM estimate billed monthly and CAM exclusions

- Base year or expense stop for gross leases

- Percentage rent clause and breakpoint if applicable

- Recovery pool participation percentage

Lease status:

- Current payment status (current, delinquent, on notice)

- Upcoming critical dates within the next 90 days

- Any pending lease modifications or active negotiations

What Are the Best Practices for Rent Roll Management?

Rent roll management best practices in real estate are not about finding the right spreadsheet format. They are about building a process that keeps the rent roll current automatically. Not depending on someone remembering to update it.

Update It at Every Lease Event, Not at Month-End

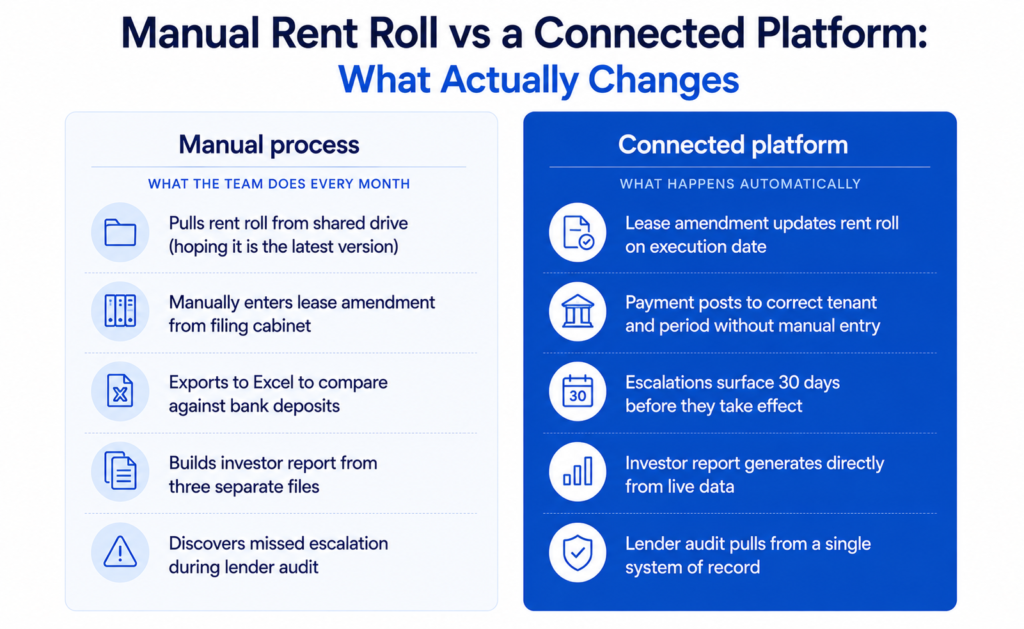

The most common rent roll management failure is treating the rent roll as a monthly report. A live document should update at every lease event, not just at period end. Every lease event changes the rent roll. New leases, renewals, amendments, escalations, free-rent periods, defaults, and terminations should all trigger an update.

Each of these should update the rent roll on the day the event occurs. Waiting for month-end creates a window where the rent roll is inaccurate. That window is when lender and investor requests most often arrive.

Know Which Escalations Are Coming Up

Rent escalations are the most commonly missed item in manual rent rolls. The escalation date passes. The rent collects at the old rate. Nobody catches it until a reconciliation or an investor review.

The best practice is to keep a forward-looking view of all upcoming escalations for the next 12 months. Every tenant whose rent changes in the next quarter should be on a review list before the change date arrives. Understanding the financial impact of how escalations are structured is worth reviewing. The breakdown of net effective rent versus face rent explains exactly how missed escalations affect the real financial value of a lease.

Check What Was Actually Collected Each Month

A rent roll that shows expected rent is only half the picture. The other half is what was actually collected. Reconciling the rent roll against bank deposits or the accounting system every month surfaces discrepancies early. Before they compound.

This reconciliation is where manual rent roll management breaks down first. When the rent roll and collections are in separate systems, reconciliation becomes a manual matching exercise. When rent payments and collections connect directly to the rent roll, the match happens automatically and exceptions surface in real time.

One Version, One Source

Rent roll version control is a persistent problem in property management. When the rent roll is an Excel file that multiple people access, version conflicts are inevitable. An amendment gets entered in one version. Someone else’s copy does not have it. Investors receive a report from the outdated version.

The solution is a single system of record. Every team member accesses it directly rather than working from a copied file, and every change should be logged with who made it and when.

Every Number Should Trace Back to a Document

The figure in the rent roll should trace back to a signed document. Base rent traces to the lease. A rent escalation traces to the escalation clause or the amendment. A CAM estimate traces to the prior year reconciliation and the current year projection.

When a lender asks how a number was derived, the answer should come from the system in seconds. Not from a search through the filing cabinet. Clean leasing and rental management processes build this traceability into the workflow from the moment a lease is executed.

What Are the Commercial Rent Roll Best Practices That Differ from Residential?

Commercial rent rolls require more fields, more calculation logic, and more ongoing attention than residential ones. The main reason is that commercial leases shift operating expenses between landlord and tenant in ways that vary by lease, by tenant, and by year. A residential rent roll tracks rent and deposit. A commercial rent roll tracks base rent, expense recovery, CAM estimates, lease type, and in some cases, a percentage of tenant sales.

Different Lease Types Need Different Columns

In a triple-net lease, the tenant pays base rent plus a share of operating expenses, property taxes, and insurance. Whereas, in a gross lease, the landlord pays expenses, and the tenant pays a fixed amount. In a modified gross lease, there is a negotiated split.

Each structure requires different rent roll columns and different calculation logic. A commercial rent roll that treats all leases as gross leases will systematically under-track recovery income from NNN tenants.

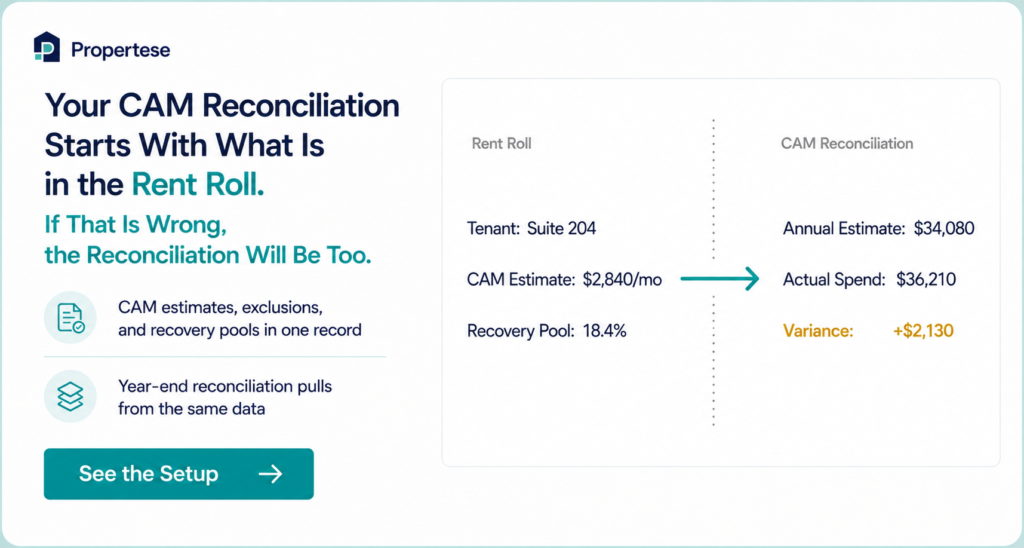

CAM Charges Belong in the Rent Roll, Not a Side File

Common area maintenance charges are often tracked separately from the rent roll in manual systems. They should not be. The rent roll should show each tenant’s monthly CAM estimate, their recovery pool participation, and their exclusions per lease.

When CAM is tracked separately, the year-end reconciliation requires pulling data from multiple places and reconciling them. When it is in the rent roll from day one, the reconciliation is a verification, not a reconstruction. For a closer look at how common area maintenance calculations connect to the financial records in practice, that page covers the recovery pool setup in detail.

Percentage Rent Needs Its Own Tracking

Tenants with percentage rent clauses pay additional rent when their sales exceed a breakpoint. Tracking this requires monitoring tenant sales reports, calculating the excess, and comparing it to the applicable percentage rate.

Most manual rent rolls do not have a column for percentage rent breakpoints. This means the landlord is depending on the tenant to self-report accurately, with no systematic check against the lease terms.

How Do You Do Rent Roll Analysis for Property Managers?

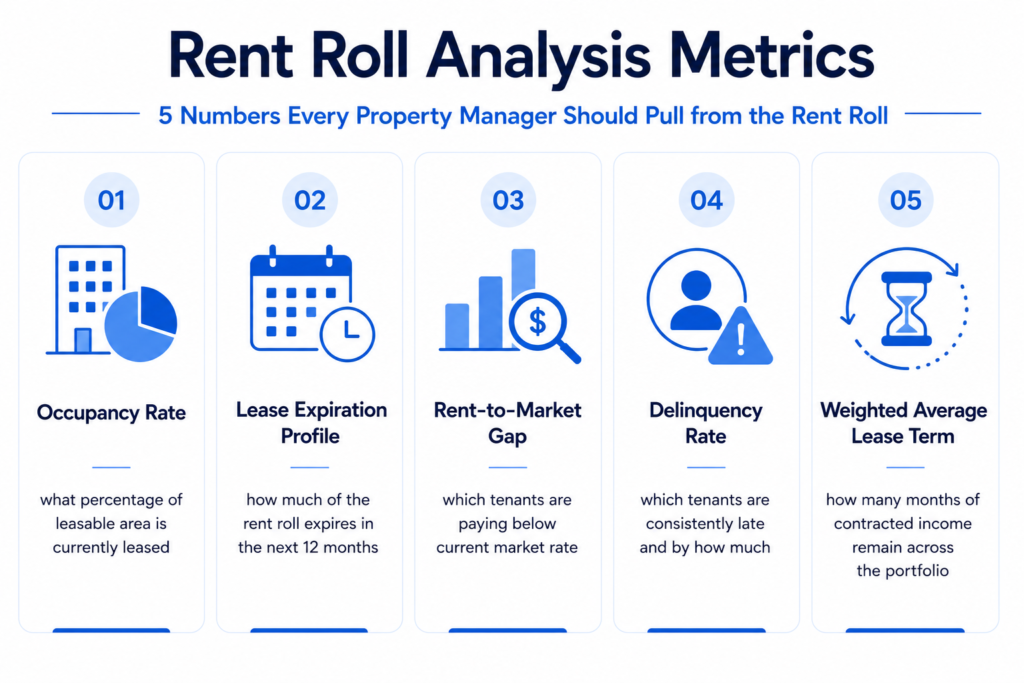

Rent roll analysis for property managers means using the rent roll to answer financial questions about the portfolio, not just to confirm who is paying what. Done well, it tells you where the risk is concentrated, which leases are coming up for renewal, and whether current rents are above or below where the market is. The metrics that matter most:

Occupancy and vacancy: What percentage of leasable area is currently occupied? What is the vacancy rate by property, by floor, by unit type?

Lease expiration profile: How much of the rent roll is expiring in the next 12 months? In the next 24? A portfolio with 40% of leases expiring in the next year has a materially different risk profile from one with expirations spread evenly over five years.

Rent-to-market comparison: Is current rent above or below market for each tenancy? Tenants paying below-market rent represent either upside on renewal or retention risk if they discover the gap.

Delinquency pattern: Which tenants are consistently late? Is the pattern concentrated in one property or one tenant type?

Renewal probability: Which leases are coming up for renewal and which tenants have exercised options previously versus allowed them to lapse?

This analysis feeds directly into financial reporting at the portfolio level. When the rent roll connects to the reporting layer, these metrics appear in real time. No manual calculation from the raw spreadsheet.

Understanding how to automate the income tracking side of this analysis reduces the monthly workload significantly. The guide on automating rental income tracking covers how this works when the payment system connects to the rent roll rather than running separately.

What Are the Best Practices for Rent Roll Reporting?

The best practice for rent roll reporting is to match the format and frequency to the audience receiving it. An internal management team needs a different view from a lender, and a lender needs a different view from an investor or an underwriter. Here is what each group typically needs.

- For internal management: A weekly exception report showing delinquencies, upcoming critical dates in the next 30 days, and any leases modified since the last report. This keeps the management team ahead of issues rather than reacting to them.

- For lenders: A complete rent roll showing every tenancy, current rent, lease term, and occupancy status. Most lenders also want to see the payment history for each tenant for the trailing 12 months. The format should match the lender’s template wherever possible to reduce back-and-forth.

- For investors: A quarterly rent roll summary showing occupancy rate, weighted average lease term, scheduled rent increases in the coming period, and a comparison of current versus market rent. Institutional investors increasingly expect this to come from the financial system directly rather than being assembled from separate exports.

- For underwriting: The most detailed format. Every lease term, every financial obligation, every rent modification since the original lease, and the status of every pending renewal or renegotiation. This is the format that takes the most time to produce manually and the most to get wrong.

When Does Rent Roll Software Become Necessary?

Rent roll software becomes necessary when a spreadsheet-based process can no longer keep the rent roll current without creating version control problems, errors, or gaps. For most portfolios, that point arrives somewhere between five and fifteen properties. It can arrive earlier if the leases are complex or if investors or lenders require regular reporting. Specific signs that the current setup is no longer working:

- More than one person needs to update the rent roll

- Investors or lenders request rent roll reports on a fixed schedule

- Commercial leases with CAM recovery require cross-referencing multiple tracking documents

- Lease amendments are frequent enough that version control becomes a problem

- Missing an escalation or a renewal deadline would have significant financial consequences

Rent roll software that connects to the general ledger closes the gap between the rent roll and the accounting system. When a lease event updates the rent roll, the financial records update at the same time. When rent is collected, the payment posts to the correct tenant and period without a manual step. The reconciliation step disappears because there is only one system.

Rent roll management best practices in real estate at scale require one platform. Lease record, rent roll, payment tracking, and financial reporting should all draw from the same data. That is the difference between a rent roll that shows what the leases say and one that shows what is actually happening financially.

Frequently Asked Questions

What is a rent roll in real estate?

A rent roll lists every tenancy in a property or portfolio. It shows current rent, lease term, and key financial terms for each tenant. It is the primary financial summary of a portfolio’s rental income capacity.

What should be included in a rent roll?

At minimum: tenant name, unit, lease dates, current rent, escalation schedule, and renewal options. Commercial rent rolls should also include lease type, CAM estimates, recovery pool participation, and any percentage rent clauses.

How often should a rent roll be updated?

Every time a lease event occurs. New leases, amendments, escalations, and renewals should all update the rent roll on the day they happen. Not at month-end.

What is the difference between a rent roll and a lease abstract?

A lease abstract extracts key terms from one lease. A rent roll aggregates summary information across every tenancy in the portfolio. Both need to be current, but the rent roll is the portfolio-level financial view.

When does spreadsheet-based rent roll management stop working?

Usually between five and fifteen properties. Or when investors require regular reports, CAM recovery becomes complex, or more than one person needs to maintain the rent roll.

What is rent roll software?

Rent roll software is a platform that tracks lease terms, rent amounts, escalations, and collections in one place. The best options connect to the general ledger so the rent roll and financial records update from the same source.

Conclusion

Rent roll management best practices in real estate all lead to the same place. When the rent roll is current and accurate, every decision that depends on it gets faster and more reliable. Lease renewals, investor reporting, lender requests. When it is not current, errors compound quietly until someone has to spend days fixing what a single update would have prevented.

If the current rent roll depends on someone remembering to update a spreadsheet after every lease event, that is the gap worth closing now.

Talk to Propertese about what rent roll management looks like when the lease record, the financial records, and the reporting layer all update from the same data.