Top 15 Property Management Tasks You Should Automate Today (With Real ROI Data)

Ever feel like you’re drowning in property management tasks? You’re not alone.

Between chasing late rent payments, coordinating maintenance requests, and keeping track of lease renewals, it’s easy to spend your entire day on admin work instead of growing your business.

But here’s the truth: Many property managers are still doing things the hard way while their competitors use automation to do more with less.

The math is simple. Every hour spent on tasks that could be automated is an hour you’re not spending on activities that actually grow your business.

Let’s look at the numbers: Property managers who implement smart automation see productivity increases of up to 40%, according to recent industry surveys. That’s like adding two extra workdays to your week without hiring anyone new.

Ready to stop working IN your business and start working ON it? Here are the 15 property management tasks you should automate today – complete with real ROI data to show you exactly what you’re leaving on the table.

1. Rent Collection and Payment Tracking

The Old Way: Manually recording rent payments, sending reminder emails, tracking down late payments, and updating spreadsheets.

The Smart Way: Implementing an automated rent collection system that sends reminders, processes payments, flags late payers, and updates your accounting system automatically.

Real ROI:

- 30% reduction in late payments

- 15+ hours saved monthly on payment processing and follow-up

- 20% improvement in cash flow predictability

Automated rent collection isn’t just convenient, it’s transformative for your bottom line. When tenants can pay online with automatic reminders, they pay faster and more consistently.

Propertese’s rent collection system integrates directly with your accounting, so every payment automatically syncs with your financial records in real-time. No more manual data entry or reconciliation headaches.

2. Maintenance Request Management

The Old Way: Taking maintenance calls at all hours, manually dispatching vendors, following up with tenants, and tracking completion status in spreadsheets.

The Smart Way: Using a maintenance portal where tenants submit requests, the system categorizes and assigns them, and status updates happen automatically.

Real ROI:

- Maintenance resolution times cut in half

- 10+ hours saved weekly on coordination and follow-up

- 25% reduction in maintenance costs through better vendor management

Efficient maintenance management isn’t just about saving time, it’s about preventing small issues from becoming expensive problems.

With Propertese’s maintenance request management system, tenants can submit requests 24/7 with photos, automatic alerts notify your team based on priority, and you get a complete digital record of all maintenance history. This means faster responses, happier tenants, and better property protection.

3. Tenant Screening and Application Processing

The Old Way: Manually reviewing applications, calling references, running credit checks separately, and coordinating with team members about decisions.

The Smart Way: Using an automated screening system that handles background checks, credit reports, and references in one streamlined process.

Real ROI:

- 75% reduction in screening time

- More consistent tenant quality (reducing costly evictions)

- 30% faster property leasing times

Finding the right tenant is crucial for long-term profitability. By automating tenant screening, you not only save time but also make more consistent decisions based on data rather than gut feeling.

4. Lease Renewals and Management

The Old Way: Manually tracking lease expiration dates, creating renewal documents, coordinating signatures, and updating records.

The Smart Way: Setting up automated renewal reminders, generating lease documents, and facilitating e-signatures through a single platform.

Real ROI:

- 35% improvement in renewal rates

- 20+ hours saved monthly on paperwork

- Significantly reduced gap periods between tenants

Lease renewals are one of the highest ROI activities in property management. Every renewal means avoiding turnover costs (which average $1,750 per unit) and maintaining consistent income.

Propertese’s lease management system automatically flags upcoming expirations, generates renewal offers based on market data, and handles the entire e-signature process, making renewals nearly effortless for both you and your tenants.

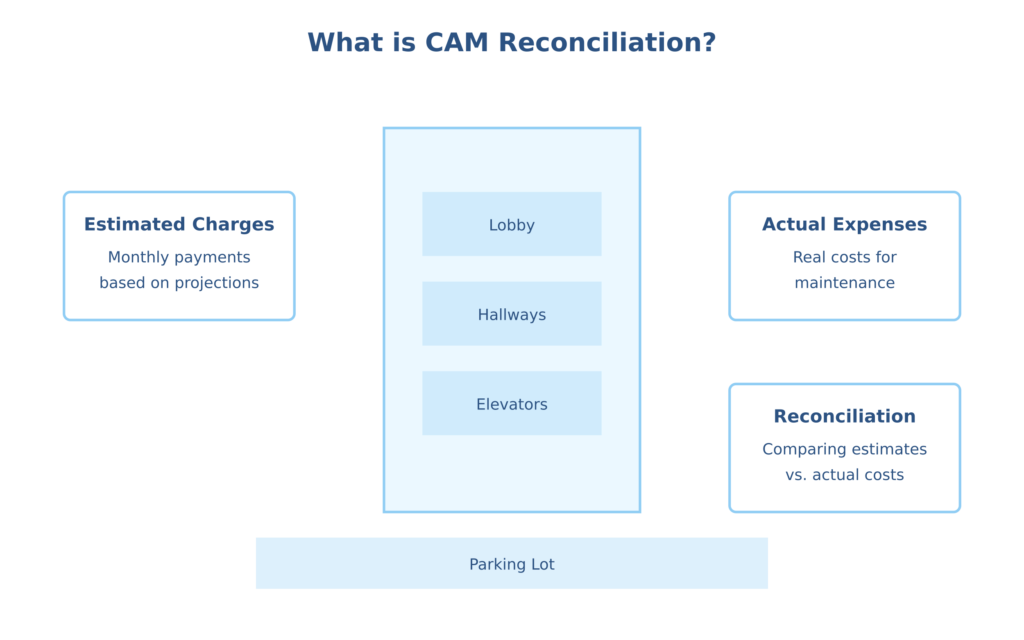

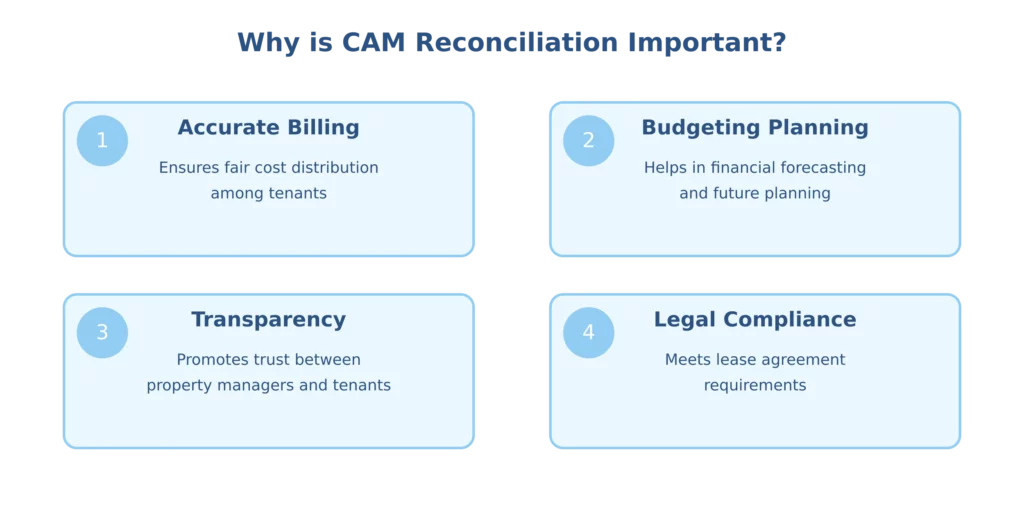

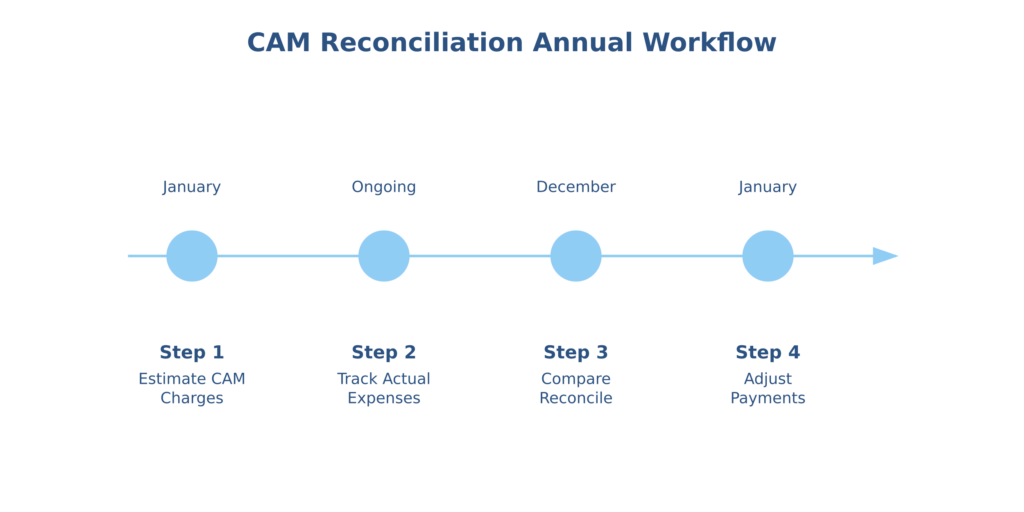

5. Financial Reporting and Analytics

The Old Way: Manually creating reports in spreadsheets, spending days compiling data for owner statements, and struggling to get real-time insights.

The Smart Way: Implementing automated financial reporting that generates real-time dashboards and owner statements with a few clicks.

Real ROI:

- 90% reduction in report creation time

- Better investment decisions through real-time data

- Increased owner satisfaction and retention

Property management is ultimately a numbers game, and those with the best data win. By automating your financial reporting, you gain both time and insight.

Propertese’s financial reporting tools pull data directly from your property activities to create real-time dashboards, owner statements, and tax reports. This means you’re always making decisions based on current information, not last month’s numbers.

6. Tenant Communication and Updates

The Old Way: Sending individual emails, making phone calls, and posting paper notices for building updates, policy changes, or announcements.

The Smart Way: Using automated messaging systems that send targeted communications to specific properties or tenant groups.

Real ROI:

- 80% reduction in communication time

- Improved tenant satisfaction through consistent updates

- Significant reduction in questions and confusion

Clear communication prevents problems before they start. Automated messaging ensures everyone gets the right information at the right time.

With Propertese’s communication tools, you can schedule announcements, segment your audience by property or lease status, and track what messages have been viewed, all from a central dashboard that integrates with your tenant data.

7. Inspection Management

The Old Way: Manually scheduling inspections, carrying clipboards and cameras, transcribing notes, and creating reports back at the office.

The Smart Way: Using digital inspection tools with built-in checklists, photo capabilities, and automated report generation.

Real ROI:

- 70% reduction in inspection time per unit

- Better documentation for liability protection

- Earlier identification of maintenance issues (saving costly repairs)

Regular inspections protect your investment, but they shouldn’t consume your week. Automation makes them fast, consistent, and actionable.

8. Vendor Management

The Old Way: Maintaining paper files of vendor contracts, manually tracking insurance certificates, and handling invoice approvals through email or paper.

The Smart Way: Implementing a vendor portal that manages documentation, automates approvals, and tracks performance metrics.

Real ROI:

- 50% reduction in vendor management time

- 15% average savings on service costs through better oversight

- Elimination of compliance risks from expired insurance

Working with quality vendors at fair prices significantly impacts your profitability. Automation helps you manage these relationships efficiently while keeping costs in check.

Propertese’s vendor management system maintains a centralized database of all your service providers, automatically flags insurance or license expirations, routes invoices for approval, and even helps you analyze which vendors deliver the best value.

9. Utility Billing and Management

The Old Way: Manually reading meters, calculating bills, creating invoices, and tracking payments for properties where owners handle utilities.

The Smart Way: Implementing automated utility billing systems that integrate with payment platforms and accounting software.

Real ROI:

- 25+ hours saved monthly on utility management

- 100% capture of billable utility costs

- Reduction in utility-related disputes with tenants

Utility billing is often overlooked but presents significant automation opportunities, especially for multi-family properties.

10. Document Management

The Old Way: Storing paper documents in filing cabinets, scanning files to email, and struggling to find the right document when needed.

The Smart Way: Implementing a cloud-based document management system with secure storage, permission controls, and instant search capabilities.

Real ROI:

- 90% reduction in document retrieval time

- Elimination of storage costs for paper documents

- Enhanced security and disaster recovery protection

Document management might not seem exciting, but the time savings and risk reduction make it a high-value automation target.

Propertese’s document management system securely stores all your leases, inspection reports, insurance documents, and communications in one searchable location. With custom permission settings, you control exactly who sees what, while maintaining an audit trail of all document activities.

11. Tenant Onboarding and Move-In

The Old Way: Manually creating welcome packets, scheduling move-in appointments, and conducting in-person orientations for each new tenant.

The Smart Way: Implementing digital onboarding with automated welcome emails, video tours, and online resources for new tenants.

Real ROI:

- 60% reduction in onboarding time per tenant

- Improved move-in experience leading to higher satisfaction

- Consistent communication of important policies and procedures

First impressions matter. A smooth, professional onboarding process sets the tone for the entire tenancy.

12. Accounting and Bookkeeping

The Old Way: Manually entering expenses, reconciling bank statements, and creating financial reports in separate systems.

The Smart Way: Implementing integrated property accounting that automates data entry, reconciliation, and financial reporting.

Real ROI:

- 20+ hours saved monthly on bookkeeping tasks

- 95% reduction in data entry errors

- Faster month-end and year-end closing

Accurate financial records are the backbone of successful property management. Automation not only saves time but also reduces costly errors.

Propertese’s accounting system is specifically designed for property management, with automated bank feeds, custom chart of accounts, and built-in reconciliation tools. The system flags unusual transactions and automatically categorizes recurring expenses, making bookkeeping almost hands-free.

13. Marketing and Listing Syndication

The Old Way: Manually posting listings on multiple websites, responding to individual inquiries, and scheduling showings through phone or email.

The Smart Way: Using a listing syndication tool that publishes to multiple platforms with automated inquiry responses and showing schedulers.

Real ROI:

- 50% reduction in vacancy periods

- 10+ hours saved weekly on marketing tasks

- Larger applicant pools leading to better tenant selection

Vacant units are profit killers. Automation helps you market properties faster and more effectively, minimizing those costly empty periods.

14. Owner Reporting and Communication

The Old Way: Creating custom reports for each owner, sending individual emails, and answering the same questions repeatedly.

The Smart Way: Implementing owner portals with on-demand reporting, automated updates, and self-service information access.

Real ROI:

- 75% reduction in owner communication time

- Higher owner satisfaction and retention

- Fewer interruptions for your team

Happy owners are loyal owners. Automation makes it easy to exceed their expectations without overwhelming your staff.

With Propertese’s owner portal, your clients can access real-time financial data, inspection reports, and other key information whenever they want. Automated monthly summaries keep them informed, while custom alerts notify them of significant events without requiring your direct involvement.

15. Compliance and Deadline Management

The Old Way: Keeping mental notes or calendar reminders for license renewals, insurance deadlines, and regulatory requirements.

The Smart Way: Implementing automated tracking for all compliance deadlines with advance notifications and status dashboards.

Real ROI:

- Virtual elimination of compliance violations and associated fines

- Protection from liability due to expired insurance or licenses

- Peace of mind from knowing nothing important will slip through the cracks

Missing important deadlines can result in fines, legal exposure, and damage to your reputation. Automation creates a safety net for these critical items.

Making the Switch: How to Implement Automation Without Disruption

If you’re still using manual processes for most of these tasks, the prospect of automating 15 different areas might seem overwhelming. The good news is that you don’t have to do everything at once.

Here’s a simple approach to implementing automation in your property management business:

- Start with high-impact, low-effort areas – Rent collection and maintenance management typically offer the biggest immediate returns.

- Choose integrated solutions – Look for platforms that handle multiple functions rather than using separate tools for each task.

- Plan for data migration – Good preparation makes the transition much smoother.

- Train your team thoroughly – Automation only delivers ROI when it’s actually used correctly.

- Measure the results – Track time savings and other benefits to calculate your actual ROI.

Why Propertese is the Smarter Way to Automate

When looking at automation options, many property managers make the mistake of cobbling together multiple single-purpose tools. This creates integration headaches, duplicate data entry, and ultimately more complexity than it solves.

Propertese offers a different approach with a comprehensive platform that handles all 15 of these automation needs in one integrated system. By centralizing your property management operations, you get:

- Seamless data flow between all functions, eliminating duplicate entry

- Consistent user experience for tenants, owners, and your team

- Single source of truth for all property information

- Lower total cost than multiple separate solutions

- Simplified training with just one system to learn

Our customers report average time savings of 15-20 hours per week per property manager after implementing Propertese. That’s like having an extra part-time employee for free.

The Real Cost of Waiting

Every day you continue with manual processes is costing you – not just in time, but in real dollars. Consider these numbers:

- Average property manager salary: $50,000/year

- Hours spent on tasks that could be automated: 20 hours/week (50% of time)

- Annual cost of manual processes: $25,000 per manager

That’s before counting opportunity costs from growth opportunities missed while handling routine tasks.

Property management automation isn’t just about efficiency, it’s about transforming your business model to achieve more with the same resources. In today’s competitive market, that’s not just nice to have, it’s essential for survival and growth.

Ready to see how Propertese can transform your property management operations? Book a demo today and discover how much time and money you can save with the right automation tools.